If you are someone you know is facing a foreclosure, this foreclosure guide will give you the information you need to help you navigate the process. Find out now the best way to prevent foreclosure.

Table of contents

- What is a foreclosure?

- Understanding The Foreclosure Process

- Foreclosure Process: Steps

- How to Delay or Stop a Foreclosure

- Foreclosure Resources

- Foreclosure Glossary Definitions

What is a foreclosure?

Foreclosure is the legal process by which a lender (the creditor) with a claim (lien) to your property attempts to collect on a debt owed by taking ownership and selling the property.

Typically, the foreclosure process is triggered when a borrower misses a certain number of payments or fails to meet the terms of the agreed mortgage contract.

The foreclosure process varies between states. There are two types of foreclosures a judicial or non-judicial. However, some states have both options.

Judicial foreclosure:

- Your mortgage lender must file suit in the court system.

- You’ll get a letter from the court demanding payment.

- Assuming the loan is valid, you’ll have 30 days to bring payment to court to avoid foreclosure (and sometimes that can be extended).

- If you don’t pay during the payment period, a judgment will be entered and the lender can request the sale of your property – usually through an auction.

- Once the property is sold, the sheriff serves an eviction notice and forces you to immediately vacate the property.

Non-judicial foreclosure (Power of sale):

- The mortgage lender serves you with papers demanding payment, and the courts are not required – although the process may be subject to judicial review.

- After the established waiting period has elapsed, a deed of trust is drawn up and control of your property is transferred to a trustee.

- The trustee can then sell your property to the lender at a public auction (notice must be given).

Understanding The Foreclosure Process

The first thing to understand about going through a foreclosure is that it’s a process, and it takes time.

According to federal law, in most cases, a lender generally cannot officially start the foreclosure process until you are behind at least 120 days in payments.

Unfortunately, you can breach the 120-day rule if you do any of the following.

The restriction applies if:

- Failed to pay property taxes if it were not in escrow

- Occupied the property if it’s stated in the mortgage contract

- If you caused excessive damage to the property lowering its value

The restriction doesn’t apply if:

- If you violated a due-on-sale clause. This allows the lender to call the note due if you transfer ownership of the property to a new person.

- If the lender is a superior or subordinate lienholder.

By law, there are steps that a lender has to take before they can take ownership of your home.

The point is you have ample time to figure out what your options are and the best actions to take to help with your situation.

The key here is to be proactive and not sit around hoping that your problem will somehow magically be solved.

Some homeowners will face foreclosure at some point. That’s just the unpredictable nature of life.

What we can do is try to help you navigate the foreclosure process, so you can move on with your life. Here are the steps for the best way to prevent foreclosure.

Foreclosure Process: Steps

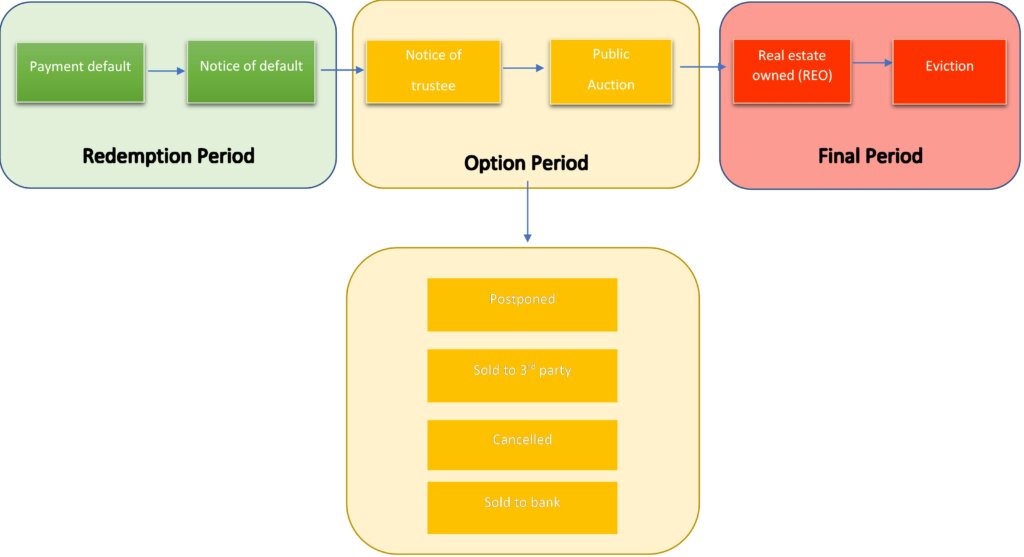

Redemption Period

This is the period after your home has been sold at a foreclosure auction. During this period you can still reclaim your home.

To get your home back, you will need to pay the outstanding mortgage balance and all costs incurred during the foreclosure process.

Payment default: A payment default occurs when the borrower misses at least one payment. The lender will notify the borrower of the missed payment.

Typically the borrower has a fifteen-day grace period before notification. However, a late fee may be assessed by the lender.

After two missed payments, the lender will typically send you a demand letter.

A demand letter or “notice to accelerate” is a professional document requesting payment of the amount that you are delinquent and that you have thirty days to bring your loan current.

If you are unable to make the full payment or negotiate terms to make the payment, your lender may proceed with the foreclosure process.

Notice of default: A notification sent by the lender stating that a payment has not been made by the predetermined deadline.

You will get this notification ninety days after your first missed payment.

During this step, the lender will hand over your loan to its foreclosure department to take over-processing.

You are still in the reinstatement period, and typically you have thirty days to settle the payment or reinstate the loan.

If you have not satisfied the outstanding balance, you will be referred to the lender’s attorneys.

You will also incur all attorney fees along with the loan delinquency amount.

Option Period

Notice of trustee’s sale: A note informing the borrower that their property will be sold at a public auction.

If you have not satisfied the loan balance or made arrangements at this point.

A notice of trustee’s sale will be filed in the county where the property is located.

The data provided will be the actual day of the foreclosure sale. You will be notified by mail, by other means or, the notice will be taped to your door.

Also, the property will be advertised for sale.

Public auction(Sherriff’s sale): The property is now up for auction and is awarded to the highest bidder.

The lender or a representative of the lender (trustee) sets the minimum bid which includes any liens, unpaid taxes, and any costs associated with the sale.

Once the auction ends, the trustee’s deed upon sale will be given to the winner.

Best Way to Prevent Foreclosure

Postponement: If you are facing a nonjudicial or Judicial foreclosure, there are a couple of options you have if you decide to try and delay the foreclosure process.

Keep in mind that these options are best suited if you work with a lawyer that fully understands the foreclosure process. Working with a lawyer is another best way to prevent foreclosure.

- Apply for loss mitigation

- Challenge the foreclosure in court

- Filing for bankruptcy

Apply for loss mitigation: This is a process used by the lender to work with buyers who are delinquent on their home loans. Loss mitigation works to negotiate the mortgage terms for the homeowner that will prevent the foreclosure from going through.

Types of loss mitigation:

- Loan modification: When the terms of the loan have been modified to help the homeowner keep their home. Common modifications are lowering the interest rate and extending the life of the loan.

- Short sale: This is the process where a lender accepts an offer for a home that is less than the principal balance.

- Deed in Lieu of foreclosure: When a homeowner signs a legal document transferring ownership of the property to the lender in exchange for being relieved of the mortgage debt.

- Special forbearance: When you are making reduced or no payments to the lender. When the forbearance period ends typically, you will pay back what you missed or, the loan will be modified.

- Partial Claim: When a lender advances funds to a homeowner in the amount necessary to reinstate a delinquent loan. However, the money advanced should not exceed the equivalent of twelve months of mortgage payments.

Challenge the foreclosure in court: If you believe you have a valid argument against a pending foreclosure, you can take the fight to your lender in court. You can file an answer in a judicial foreclosure or file your own suit to fight a non-judicial foreclosure.

File for bankruptcy: You can stop or delay a foreclosure by filing for chapter 7 or chapter 13 bankruptcy.

You can use chapter 7 bankruptcy to save your home if you are current on your payments. If not, it will only delay the process.

Chapter 13 bankruptcy will be a better option if your goal is to keep the home. You will be able to pay your delinquent balance over the span of three to five years.

Note: Keep in mind that filing for bankruptcy will hurt your capacity to borrow in the future.

Sell to a 3rd party: If you are going through the option period and you’re running out of viable options. Selling your home through a realtor on the Mulitple listing service (MLS) can be great.

However, what if your home isn’t in tip-top shape, is rough around the edges, or needs major improvements before going on the market.

You can try selling directly to an investor it might work for you.

This option isn’t for everyone and not all situations, but it can work given your circumstances.

If you’re on the fence on whether working with an investor might be a good choice.

Check out these two articles for insight into the pros and cons of selling your home to an investor. Selling your home to an investor can be one of the best ways to prevent foreclosure.

Related article:

Pros of We Buy Houses Companies

Cons of We Buy Houses Companies

Get the foreclosure canceled: You can get the foreclosure process canceled by reaching an agreement with your lender, having a short sale, selling to a 3rd party, or filing for bankruptcy.

Sell your home back to the bank: You can sell your home back to the bank by using a deed in lieu of foreclosure. Keep in mind that this option will negatively affect your credit.

Final Period

Real estate owned(REO): After an unsuccessful sale at the county auction, the property is now in the ownership of the lender.

The property is listed on the lender’s books as (REO) also called “bank owned” and is categorized as an asset.

The lender will attempt to sell the property through a broker or with an asset manager.

Typically you will see these homes advertised for sale as foreclosures on Zillow.com, HAR.com, Realtor.com, Foreclosure.com, and other multiple listing services(MLS).

Eviction: This is the point of little to no return. Sometimes the borrow can stay in the home for a short period.

Eventually, local law enforcement will be called to execute the eviction notice.

Unfortunately, if you are still there you, and your possessions will be removed from the home. ▲ 1

Best Way to Prevent Foreclosure: Resources

There are many government programs that are available to assist homeowners at risk of foreclosure. Beginning with contacting a HUD-approved counselor near you or call HUD at (800)569-4287 They can stare you in the right direction on the best way to prevent foreclosure

Below are the following programs that can be found at hud.gov

Modify or refinance your loan:

- Home Affordable Modification Program (HAMP): HAMP lowers your monthly mortgage payment to 31 percent of your verified monthly gross (pre-tax) income to make your payments more affordable. The typical HAMP modification results in a 40 percent drop in a monthly mortgage payment. Eighteen percent of HAMP homeowners reduce their payments by $1,000 or more.

- Principal Reduction Alternative (PRA): PRA was designed to help homeowners whose homes are worth significantly less than they owe by encouraging servicers and investors to reduce the amount they owe on their homes.

- Second Lien Modification Program (2MP): If your first mortgage was permanently modified under HAMP SM and you have a second mortgage on the same property, you may be eligible for a modification or principal reduction on your second mortgage under 2MP. Likewise, If you have a home equity loan, HELOC, or some other second lien that is making it difficult for you to keep up with your mortgage payments, learn more about this MHA program.

- Home Affordable Refinance Program (HARP): If you are current on your mortgage and have been unable to obtain a traditional refinance because the value of your home has declined, you may be eligible to refinance through HARP. HARP is designed to help you refinance into a new affordable, more stable mortgage.

Unemployed Homeowners:

- Home Affordable Unemployment Program (UP): If you are having a tough time making your mortgage payments because you are unemployed, you may be eligible for UP. UP provides a temporary reduction or suspension of mortgage payments for at least twelve months while you seek re-employment.

- Emergency Homeowners’ Loan Program (EHLP):

- FHA Special Forbearance: If you are having difficulty making mortgage payments because you are unemployed and have no other sources of income, you may be eligible for FHA’s Special Forbearance. FHA now requires servicers to extend the forbearance period, by offering a reduced or suspended mortgage payment for up to twelve months, for FHA borrowers who qualify for the program.

Underwater Mortgages:

In today’s housing market, many homeowners have experienced a decrease in their home’s value. Learn about these MHA programs to address this concern for homeowners.

- Home Affordable Refinance Program (HARP): If you are current on your mortgage and have been unable to obtain a traditional refinance because the value of your home has declined, you may be eligible to refinance through HARP. HARP is designed to help you refinance into a new affordable, more stable mortgage.

- Principal Reduction Alternative: PRA was designed to help homeowners whose homes are worth significantly less than they owe by encouraging servicers and investors to reduce the amount you owe on your home.

- Treasury/FHA Second Lien Program (FHA2LP): If you have a second mortgage and the mortgage servicer of your first mortgage agrees to participate in FHA Short Refinance, you may qualify to have your second mortgage on the same home reduced or eliminated through FHA2LP. If the servicer of your second mortgage agrees to participate, the total amount of your mortgage debt after the refinance cannot exceed 115% of your home’s current value.

Best Way to Prevent Foreclosure: Glossary Definitions

Adjustable-Rate Mortgage (ARM): Loan in which interest rate will change periodically.

Agreement of Sale: Document containing the terms and conditions for the transfer of a property’s ownership.

Appraisal: A document from a professional that gives an estimate of a property’s fair market value.

As-is: Selling a property in its current state.

Bankruptcy: The legal process by which people or entities who cannot pay their debts seek relief from some or all of their debts.

Closing Cost: Fees associated with the purchase of a home. The fees are typically 2-5 percent of the home price.

Deed: Legal document that shows the transfer of ownership of a property from one person to another.

Deed of Trust: A real estate transaction document used when a party has taken a loan from another to purchase a property.

Deed-in-Lieu: When a homeowner signs a legal document transferring ownership of the property to the lender in exchange for being relieved of the mortgage debt.

Default: Failure to make a mortgage payment within a specific time.

Demand Letter: A professional document requesting payment of the amount that you are delinquent and that you have thirty days to bring your loan current.

Depreciation: When your property value goes down.

Distressed Property: Properties that are physically in poor condition or underwater financially.

Equity: The difference between the fair market value of the property in comparison to the amount owed on the loan.

Escrow: A financial institution holds money on behalf of two parties while processing a transaction.

Eviction: The legal process of removing a person from a property.

Fannie Mae: Federal National Mortgage Association, is a government-sponsored enterprise that purchases and guarantees mortgages through the secondary market.

Federal Housing Administration(FHA): Provides mortgage insurance on loans made by FHA-approved lenders.

Foreclosure: Foreclosure is the legal process by which a lender (the creditor) with a claim (lien) to your property attempts to collect on a debt owed by taking ownership and selling the property.

Forbearance: Temporary postponement of mortgage payments.

Fix-Rate Mortgage: The same interest rate throughout the entire loan.

Home Equity Loan: When a homeowner borrows against the equity in their property.

Housing Counselor: Qualified person approved by U.S Department of Housing and Urban Development (HUD)

Junior Mortgage: Also referred to as a second mortgage, its the subordinate to the senior mortgage (first mortgage)

Lender: Person or entity that lends money to a borrower.

Lien: A legal claim against a property to satisfy a debt.

Loan Modification: When the terms of the loan have been modified to help the homeowner keep their home. Common modifications are lowering the interest rate and extending the life of the loan.

Market Value: The price at which a property would sell for in a fair market.

Modification: The process where your lender changes one or more terms of the mortgage contract.

Note: Legal document obligating a borrower to repay a mortgage loan at a set interest rate for a period of time.

Notice of Default: Notification sent by the lender stating that a payment has not been made by the predetermined deadline.

Notice of Pre-Foreclosure: Legal notice informing you that the lender has begun the process of foreclosure.

Notice of Trustee’s Sale: A note informing the borrower that the property will be sold at a public auction.

Owner Occupied: When you reside in a property.

Owner Financing: When a homeowner finances part or all of the sale of a property.

Power of Attorney: A legal document authorizing another person to act on your behalf.

Pre-foreclosure: The first set in the foreclosure process is designed to give the homeowner options to remain in their home.

Principal: The amount owed on your loan.

Principal, Interest, Taxes, and Insurance (PITI): The total amount a homeowner is responsible for monthly.

Quitclaim deed: Legal document transferring ownership of a property.

Real Estate Owned: Property unsuccessfully sold at an auction.

Refinance: Revision of the terms of a loan such as interest rate, payment date, or other terms. The new mortgage on the loan has no change in ownership.

Reinstatement: Restoring to the original terms of the mortgage agreement after the filing of a foreclosure.

Tax Lien: Hold placed on a property due to unpaid taxes.

Title: Document that shows who is the owner of the property.

Title Search: Obtaining current and historical records of a property.

Trustee: Neutral party who advertises and conducts the sale of foreclosure.

Trustee’s Deed Upon Sale: The process of transferring property after the filing of a foreclosure.

Variable Interest Rate: The interest rate that varies over a period of time.

Wraparound Mortgage: A new loan that includes the existing loan.

Best Way to Prevent Foreclosure: Conclusion

This article will give you the best way to prevent foreclosure. We walk you through all the different steps of the foreclosure process and how you can avoid it. If you find yourself behind on your mortgage and you don’t know where to turn. Read this blog post and we are almost certain you will find the information you need.

If you are someone you know is facing a foreclosure, this foreclosure guide will give you the information you need to help you navigate the process. Find out now the best way to prevent foreclosure.

Table of contents

- What is a foreclosure?

- Understanding The Foreclosure Process

- Foreclosure Process: Steps

- How to Delay or Stop a Foreclosure

- Foreclosure Resources

- Foreclosure Glossary Definitions

What is a foreclosure?

Foreclosure is the legal process by which a lender (the creditor) with a claim (lien) to your property attempts to collect on a debt owed by taking ownership and selling the property.

Typically, the foreclosure process is triggered when a borrower misses a certain number of payments or fails to meet the terms of the agreed mortgage contract.

The foreclosure process varies between states. There are two types of foreclosures a judicial or non-judicial. However, some states have both options.

Judicial foreclosure:

- Your mortgage lender must file suit in the court system.

- You’ll get a letter from the court demanding payment.

- Assuming the loan is valid, you’ll have 30 days to bring payment to court to avoid foreclosure (and sometimes that can be extended).

- If you don’t pay during the payment period, a judgment will be entered and the lender can request the sale of your property – usually through an auction.

- Once the property is sold, the sheriff serves an eviction notice and forces you to immediately vacate the property.

Non-judicial foreclosure (Power of sale):

- The mortgage lender serves you with papers demanding payment, and the courts are not required – although the process may be subject to judicial review.

- After the established waiting period has elapsed, a deed of trust is drawn up and control of your property is transferred to a trustee.

- The trustee can then sell your property to the lender at a public auction (notice must be given).

Understanding The Foreclosure Process

The first thing to understand about going through a foreclosure is that it’s a process, and it takes time.

According to federal law, in most cases, a lender generally cannot officially start the foreclosure process until you are behind at least 120 days in payments.

Unfortunately, you can breach the 120-day rule if you do any of the following.

The restriction applies if:

- Failed to pay property taxes if it were not in escrow

- Occupied the property if it’s stated in the mortgage contract

- If you caused excessive damage to the property lowering its value

The restriction doesn’t apply if:

- If you violated a due-on-sale clause. This allows the lender to call the note due if you transfer ownership of the property to a new person.

- If the lender is a superior or subordinate lienholder.

By law, there are steps that a lender has to take before they can take ownership of your home.

The point is you have ample time to figure out what your options are and the best actions to take to help with your situation.

The key here is to be proactive and not sit around hoping that your problem will somehow magically be solved.

Some homeowners will face foreclosure at some point. That’s just the unpredictable nature of life.

What we can do is try to help you navigate the foreclosure process, so you can move on with your life. Here are the steps for the best way to prevent foreclosure.

Foreclosure Process: Steps

Redemption Period

This is the period after your home has been sold at a foreclosure auction. During this period you can still reclaim your home.

To get your home back, you will need to pay the outstanding mortgage balance and all costs incurred during the foreclosure process.

Payment default: A payment default occurs when the borrower misses at least one payment. The lender will notify the borrower of the missed payment.

Typically the borrower has a fifteen-day grace period before notification. However, a late fee may be assessed by the lender.

After two missed payments, the lender will typically send you a demand letter.

A demand letter or “notice to accelerate” is a professional document requesting payment of the amount that you are delinquent and that you have thirty days to bring your loan current.

If you are unable to make the full payment or negotiate terms to make the payment, your lender may proceed with the foreclosure process.

Notice of default: A notification sent by the lender stating that a payment has not been made by the predetermined deadline.

You will get this notification ninety days after your first missed payment.

During this step, the lender will hand over your loan to its foreclosure department to take over-processing.

You are still in the reinstatement period, and typically you have thirty days to settle the payment or reinstate the loan.

If you have not satisfied the outstanding balance, you will be referred to the lender’s attorneys.

You will also incur all attorney fees along with the loan delinquency amount.

Option Period

Notice of trustee’s sale: A note informing the borrower that their property will be sold at a public auction.

If you have not satisfied the loan balance or made arrangements at this point.

A notice of trustee’s sale will be filed in the county where the property is located.

The data provided will be the actual day of the foreclosure sale. You will be notified by mail, by other means or, the notice will be taped to your door.

Also, the property will be advertised for sale.

Public auction(Sherriff’s sale): The property is now up for auction and is awarded to the highest bidder.

The lender or a representative of the lender (trustee) sets the minimum bid which includes any liens, unpaid taxes, and any costs associated with the sale.

Once the auction ends, the trustee’s deed upon sale will be given to the winner.

Best Way to Prevent Foreclosure

Postponement: If you are facing a nonjudicial or Judicial foreclosure, there are a couple of options you have if you decide to try and delay the foreclosure process.

Keep in mind that these options are best suited if you work with a lawyer that fully understands the foreclosure process. Working with a lawyer is another best way to prevent foreclosure.

- Apply for loss mitigation

- Challenge the foreclosure in court

- Filing for bankruptcy

Apply for loss mitigation: This is a process used by the lender to work with buyers who are delinquent on their home loans. Loss mitigation works to negotiate the mortgage terms for the homeowner that will prevent the foreclosure from going through.

Types of loss mitigation:

- Loan modification: When the terms of the loan have been modified to help the homeowner keep their home. Common modifications are lowering the interest rate and extending the life of the loan.

- Short sale: This is the process where a lender accepts an offer for a home that is less than the principal balance.

- Deed in Lieu of foreclosure: When a homeowner signs a legal document transferring ownership of the property to the lender in exchange for being relieved of the mortgage debt.

- Special forbearance: When you are making reduced or no payments to the lender. When the forbearance period ends typically, you will pay back what you missed or, the loan will be modified.

- Partial Claim: When a lender advances funds to a homeowner in the amount necessary to reinstate a delinquent loan. However, the money advanced should not exceed the equivalent of twelve months of mortgage payments.

Challenge the foreclosure in court: If you believe you have a valid argument against a pending foreclosure, you can take the fight to your lender in court. You can file an answer in a judicial foreclosure or file your own suit to fight a non-judicial foreclosure.

File for bankruptcy: You can stop or delay a foreclosure by filing for chapter 7 or chapter 13 bankruptcy.

You can use chapter 7 bankruptcy to save your home if you are current on your payments. If not, it will only delay the process.

Chapter 13 bankruptcy will be a better option if your goal is to keep the home. You will be able to pay your delinquent balance over the span of three to five years.

Note: Keep in mind that filing for bankruptcy will hurt your capacity to borrow in the future.

Sell to a 3rd party: If you are going through the option period and you’re running out of viable options. Selling your home through a realtor on the Mulitple listing service (MLS) can be great.

However, what if your home isn’t in tip-top shape, is rough around the edges, or needs major improvements before going on the market.

You can try selling directly to an investor it might work for you.

This option isn’t for everyone and not all situations, but it can work given your circumstances.

If you’re on the fence on whether working with an investor might be a good choice.

Check out these two articles for insight into the pros and cons of selling your home to an investor. Selling your home to an investor can be one of the best ways to prevent foreclosure.

Related article:

Pros of We Buy Houses Companies

Cons of We Buy Houses Companies

Get the foreclosure canceled: You can get the foreclosure process canceled by reaching an agreement with your lender, having a short sale, selling to a 3rd party, or filing for bankruptcy.

Sell your home back to the bank: You can sell your home back to the bank by using a deed in lieu of foreclosure. Keep in mind that this option will negatively affect your credit.

Final Period

Real estate owned(REO): After an unsuccessful sale at the county auction, the property is now in the ownership of the lender.

The property is listed on the lender’s books as (REO) also called “bank owned” and is categorized as an asset.

The lender will attempt to sell the property through a broker or with an asset manager.

Typically you will see these homes advertised for sale as foreclosures on Zillow.com, HAR.com, Realtor.com, Foreclosure.com, and other multiple listing services(MLS).

Eviction: This is the point of little to no return. Sometimes the borrow can stay in the home for a short period.

Eventually, local law enforcement will be called to execute the eviction notice.

Unfortunately, if you are still there you, and your possessions will be removed from the home.

Best Way to Prevent Foreclosure: Resources

There are many government programs that are available to assist homeowners at risk of foreclosure. Beginning with contacting a HUD-approved counselor near you or call HUD at (800)569-4287 They can stare you in the right direction on the best way to prevent foreclosure

Below are the following programs that can be found at hud.gov

Modify or refinance your loan:

- Home Affordable Modification Program (HAMP): HAMP lowers your monthly mortgage payment to 31 percent of your verified monthly gross (pre-tax) income to make your payments more affordable. The typical HAMP modification results in a 40 percent drop in a monthly mortgage payment. Eighteen percent of HAMP homeowners reduce their payments by $1,000 or more.

- Principal Reduction Alternative (PRA): PRA was designed to help homeowners whose homes are worth significantly less than they owe by encouraging servicers and investors to reduce the amount they owe on their homes.

- Second Lien Modification Program (2MP): If your first mortgage was permanently modified under HAMP SM and you have a second mortgage on the same property, you may be eligible for a modification or principal reduction on your second mortgage under 2MP. Likewise, If you have a home equity loan, HELOC, or some other second lien that is making it difficult for you to keep up with your mortgage payments, learn more about this MHA program.

- Home Affordable Refinance Program (HARP): If you are current on your mortgage and have been unable to obtain a traditional refinance because the value of your home has declined, you may be eligible to refinance through HARP. HARP is designed to help you refinance into a new affordable, more stable mortgage.

Unemployed Homeowners:

- Home Affordable Unemployment Program (UP): If you are having a tough time making your mortgage payments because you are unemployed, you may be eligible for UP. UP provides a temporary reduction or suspension of mortgage payments for at least twelve months while you seek re-employment.

- Emergency Homeowners’ Loan Program (EHLP):

- FHA Special Forbearance: If you are having difficulty making mortgage payments because you are unemployed and have no other sources of income, you may be eligible for FHA’s Special Forbearance. FHA now requires servicers to extend the forbearance period, by offering a reduced or suspended mortgage payment for up to twelve months, for FHA borrowers who qualify for the program.

Underwater Mortgages:

In today’s housing market, many homeowners have experienced a decrease in their home’s value. Learn about these MHA programs to address this concern for homeowners.

- Home Affordable Refinance Program (HARP): If you are current on your mortgage and have been unable to obtain a traditional refinance because the value of your home has declined, you may be eligible to refinance through HARP. HARP is designed to help you refinance into a new affordable, more stable mortgage.

- Principal Reduction Alternative: PRA was designed to help homeowners whose homes are worth significantly less than they owe by encouraging servicers and investors to reduce the amount you owe on your home.

- Treasury/FHA Second Lien Program (FHA2LP): If you have a second mortgage and the mortgage servicer of your first mortgage agrees to participate in FHA Short Refinance, you may qualify to have your second mortgage on the same home reduced or eliminated through FHA2LP. If the servicer of your second mortgage agrees to participate, the total amount of your mortgage debt after the refinance cannot exceed 115% of your home’s current value.

Best Way to Prevent Foreclosure: Glossary Definitions

Adjustable-Rate Mortgage (ARM): Loan in which interest rate will change periodically.

Agreement of Sale: Document containing the terms and conditions for the transfer of a property’s ownership.

Appraisal: A document from a professional that gives an estimate of a property’s fair market value.

As-is: Selling a property in its current state.

Bankruptcy: The legal process by which people or entities who cannot pay their debts seek relief from some or all of their debts.

Closing Cost: Fees associated with the purchase of a home. The fees are typically 2-5 percent of the home price.

Deed: Legal document that shows the transfer of ownership of a property from one person to another.

Deed of Trust: A real estate transaction document used when a party has taken a loan from another to purchase a property.

Deed-in-Lieu: When a homeowner signs a legal document transferring ownership of the property to the lender in exchange for being relieved of the mortgage debt.

Default: Failure to make a mortgage payment within a specific time.

Demand Letter: A professional document requesting payment of the amount that you are delinquent and that you have thirty days to bring your loan current.

Depreciation: When your property value goes down.

Distressed Property: Properties that are physically in poor condition or underwater financially.

Equity: The difference between the fair market value of the property in comparison to the amount owed on the loan.

Escrow: A financial institution holds money on behalf of two parties while processing a transaction.

Eviction: The legal process of removing a person from a property.

Fannie Mae: Federal National Mortgage Association, is a government-sponsored enterprise that purchases and guarantees mortgages through the secondary market.

Federal Housing Administration(FHA): Provides mortgage insurance on loans made by FHA-approved lenders.

Foreclosure: Foreclosure is the legal process by which a lender (the creditor) with a claim (lien) to your property attempts to collect on a debt owed by taking ownership and selling the property.

Forbearance: Temporary postponement of mortgage payments.

Fix-Rate Mortgage: The same interest rate throughout the entire loan.

Home Equity Loan: When a homeowner borrows against the equity in their property.

Housing Counselor: Qualified person approved by U.S Department of Housing and Urban Development (HUD)

Junior Mortgage: Also referred to as a second mortgage, its the subordinate to the senior mortgage (first mortgage)

Lender: Person or entity that lends money to a borrower.

Lien: A legal claim against a property to satisfy a debt.

Loan Modification: When the terms of the loan have been modified to help the homeowner keep their home. Common modifications are lowering the interest rate and extending the life of the loan.

Market Value: The price at which a property would sell for in a fair market.

Modification: The process where your lender changes one or more terms of the mortgage contract.

Note: Legal document obligating a borrower to repay a mortgage loan at a set interest rate for a period of time.

Notice of Default: Notification sent by the lender stating that a payment has not been made by the predetermined deadline.

Notice of Pre-Foreclosure: Legal notice informing you that the lender has begun the process of foreclosure.

Notice of Trustee’s Sale: A note informing the borrower that the property will be sold at a public auction.

Owner Occupied: When you reside in a property.

Owner Financing: When a homeowner finances part or all of the sale of a property.

Power of Attorney: A legal document authorizing another person to act on your behalf.

Pre-foreclosure: The first set in the foreclosure process is designed to give the homeowner options to remain in their home.

Principal: The amount owed on your loan.

Principal, Interest, Taxes, and Insurance (PITI): The total amount a homeowner is responsible for monthly.

Quitclaim deed: Legal document transferring ownership of a property.

Real Estate Owned: Property unsuccessfully sold at an auction.

Refinance: Revision of the terms of a loan such as interest rate, payment date, or other terms. The new mortgage on the loan has no change in ownership.

Reinstatement: Restoring to the original terms of the mortgage agreement after the filing of a foreclosure.

Tax Lien: Hold placed on a property due to unpaid taxes.

Title: Document that shows who is the owner of the property.

Title Search: Obtaining current and historical records of a property.

Trustee: Neutral party who advertises and conducts the sale of foreclosure.

Trustee’s Deed Upon Sale: The process of transferring property after the filing of a foreclosure.

Variable Interest Rate: The interest rate that varies over a period of time.

Wraparound Mortgage: A new loan that includes the existing loan.

Best Way to Prevent Foreclosure: Conclusion

This article will give you the best way to prevent foreclosure. We walk you through all the different steps of the foreclosure process and how you can avoid it. If you find yourself behind on your mortgage and you don’t know where to turn. Read this blog post and we are almost certain you will find the information you need.